1. Take Inventory of Your Assets and Debts

Start by listing everything you own and owe. This includes tangible assets like your home, vehicles, and other personal belongings, as well as intangible assets like bank accounts, investments, retirement accounts, insurance policies, and debts.

Write down details of each: Descriptions, locations, years acquired, current estimated value, legal descriptions, or other identifying features depending on the asset/item/property.

2. Articulate Your Goals

Consider what you want your legacy to reflect. Defining your goals is a foundational step in giving your wishes a tangible form. Clarity on this can be foundational to help inform the more technical estate planning decisions.

Are you focused on providing for loved ones, leaving a charitable legacy, addressing potential estate taxes, or a combination of these? The details and specifics matter.

3. Choose Your Beneficiaries

Decide who will inherit your assets and how they will be distributed. Be specific in outlining your wishes to avoid misunderstandings. Beneficiaries can include your spouse, children, other family members, friends, or charitable organizations.

4. Enlist Expert Guidance

Seek advice from professionals such as estate planning attorneys, financial advisors, and tax professionals. These experts can help you understand your options, craft a plan tailored to your situation, and take some of the burden off you. They also can help to identify potential pitfalls to avoid and keep you compliant with legal requirements.

5. Review and Update Regularly

Life events or changes in your financial situation may warrant a review of your estate plan. Events like marriage, divorce, a birth in the family, a death in the family, a significant inheritance, or relocation may require updates to your plan. Regular reviews and updates can address these changes and keep your plan relevant to your life as it evolves.

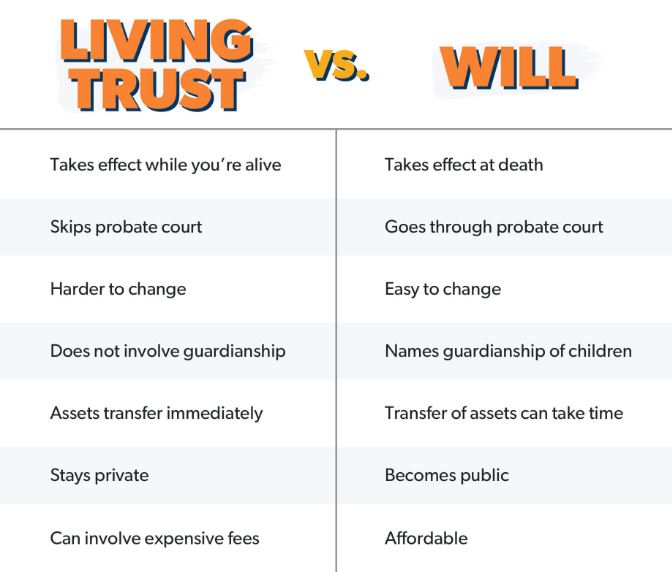

Wills

A will only takes effect after death and outlines how your assets are to be distributed, who will be the guardian of your children, and who you appoint to handle your final affairs. Without a will, the courts make these decisions.

A will is effective only after death and serves as a roadmap for asset distribution, guardianship of children, and appointment of an executor.

Trusts

Unlike a Will, Trusts can be established and implemented during your lifetime and offer more control over asset distribution. They are particularly useful for managing assets if you become incapacitated and can provide tax benefits, control, and privacy that wills do not.

Pros and Cons of Each – A Side-by-Side Comparison

Scenarios where one might be more suitable than the other

- Wills can be sufficient if your estate is relatively simple, your main concern is ensuring your assets are distributed according to your wishes, and you don’t mind putting your beneficiaries through the probate process.

- Trusts are better suited for more complex estates, if you want to avoid probate, add a layer of privacy, or want to plan for potential incapacity. Trusts can also be valuable if you have specific conditions for how and when beneficiaries receive their inheritance, such as in the case of minor children or family members with special needs.

Benefits of consulting with estate planning professionals

Estate planning is complex, and seeking the guidance of experienced professionals can make your life easier. These professionals are your allies. They can guide you through this process, providing valuable support every step of the way.

- Financial advisors –Can be your main point of contact on all financial considerations, and help you align all financial decisions with your values, goals, and needs.

- Tax Professionals – Can identify and help you implement tax strategies before during and after the estate planning process.

- Estate Attorneys – Will actually write up the documents and implement your estate plan. Ideally, prior to doing so, they will confirm the details of your goals, needs, and wishes.

How to choose the right professional for your needs

The two main considerations for choosing the right professionals are:

- Their level of competence.

- Your trust in them.

Beyond that though:

- We recommend advisors that work in a holistic, fiduciary capacity.

- We recommend CPAs that engage in long-term tax planning rather than simply filing tax returns.

- We recommend Attorneys that take the time to:

- Understand your situation and your desires

- Explain the details of each core aspect of the documents

- Draft very thorough legal documents

Recap of The Importance of Estate Planning

Estate planning is the framework for creating legal protections that honor your final wishes. This process begins with thoughtful preparation, often before a consultation with an attorney, where you define your goals, assess your overall finances, and consider the lasting impact you’d like to build.

Being proactive rather than reactive in this area is a massive gift to those who matter most to you.

Encouragement to Take the Next Step

Don’t worry about having all the answers or preparing for every eventuality just yet.

Taking the first step toward estate planning is simply an assessment of your current situation and your future goals. Start where you are and take the time to thoughtfully shape your plan. By starting with one step at a time, you can gain clarity without overwhelming yourself with every detail.

Ultimately, estate planning is a pathway to leaving a legacy for your loved ones that can last long after you’re gone.